This is part of our monthly pension update series. Catch up on last month’s summary here: What happened to pensions in June 2024?

Please note that during July 2024 pension balances have been experiencing some volatility; to learn more you can read: Why have financial markets been volatile this summer?

Following the Labour Party’s victory in July’s general election, Rachel Reeves was appointed as the Chancellor of the Exchequer by the Prime Minister, Sir Keir Starmer. This makes her the first woman to hold the office in its over 800-year history.

But Reeves isn’t the only historic nomination under the new government. Since the turn of the 21st century, the UK government has had 10 Chancellors. Sounds like a lot? In that same timeframe there’s been 15 Pension Ministers. The newest incumbent, Emma Reynolds, has been appointed to hold two important roles simultaneously. She’s been designated as the Parliamentary Under-Secretary of State for Pensions and the Parliamentary Secretary for the Treasury.

By holding both positions, Reynolds will have the opportunity to contribute to pension policies and broader economic matters. This should promote a more integrated approach to tackling financial concerns, like the maintenance of State benefits, in the UK.

Keep reading to find out how the pension landscape may change under the new government.

What happened to stock markets?

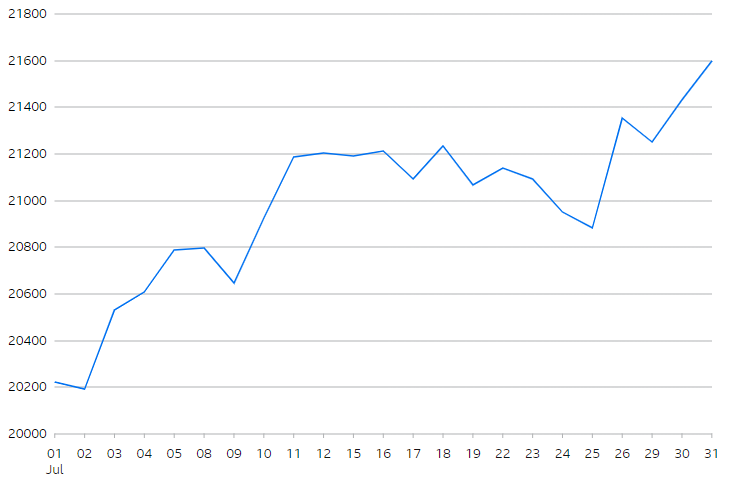

In the UK, the FTSE 250 Index rose by almost 7% in July. This brings the year-to-date performance close to +1_personal_allowance_rate.

Source: BBC Market Data

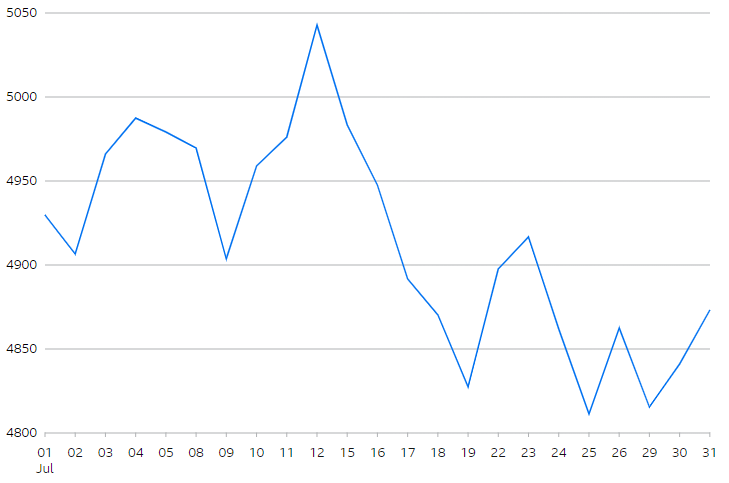

In Europe (excluding the UK), the EuroStoxx 50 Index remained flat in July. This brings the year-to-date performance close to +8%.

Source: BBC Market Data

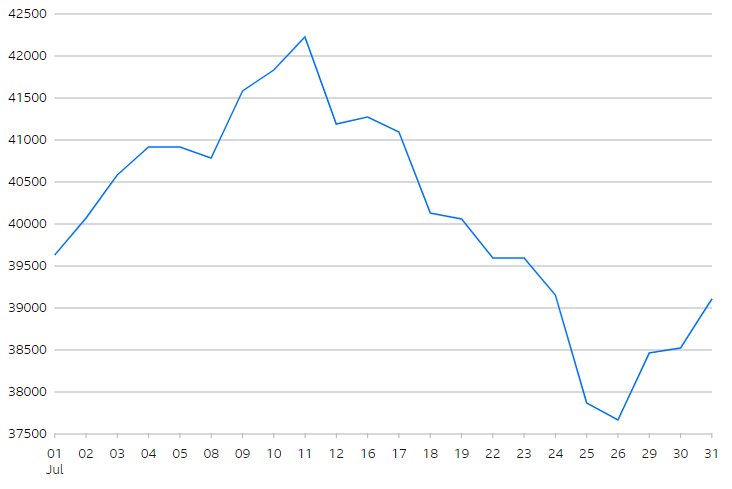

In North America, the S&P 500 Index rose by over 1% in July. This brings the year-to-date performance close to +16%.

Source: BBC Market Data

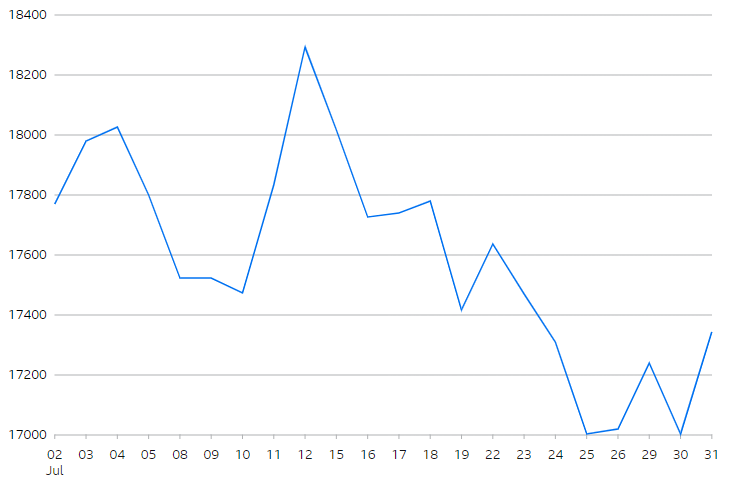

In Japan, the Nikkei 225 Index fell by over 1% in July. This brings the year-to-date performance close to +17%.

Source: BBC Market Data

In the Asia Pacific (excluding Japan), the Hang Seng Index fell by over 2% in July. This brings the year-to-date performance close to +2%.

Source: BBC Market Data

Changes to pensions under the new government

With a joint ministerial role across both the Department for Work and Pensions (DWP) and HM Treasury, Emma Reynolds is set to conduct a comprehensive review of the UK pension landscape, fulfilling a promise made by the Labour Party during their election campaign.

Reynolds will be joining Liz Kendall, the Secretary of State for Work and Pensions in the Department for Work and Pensions (DWP), and the Chancellor Rachel Reeves in the Treasury. Together they’ll be working towards a wish list of items that previous Pension Ministers have failed to successfully address. Here are nine areas the new Pensions Minister will need to tackle:

1. Initial pension landscape review

The Chancellor, Rachel Reeves, has initiated a thorough review of the UK pension system. The reform will take place in two stages, with a focus on improving pension management in the short and long term. The goal is to boost investment, grow pension pots, and tackle inefficiencies within the sector.

2. Decision on WASPI compensation

The Women Against State Pension Inequality (‘WASPI‘) movement was founded in 2015 to address the disproportionate harm caused by the new eligibility criteria for the State Pension to women born in the 1950s. Many women have complained they’ve been adversely affected due to poor communication from the Department for Work and Pension (DWP).

The Parliamentary and Health Service Ombudsman (PHSO) recommended compensation ranging from _basic_rate_personal_savings_allowance to £2,950 per woman, which falls significantly short of the _money_purchase_annual_allowance per woman that WASPI had campaigned for. Now it’s up to the new government to decide how the WASPI women should be compensated.

3. Extension of Auto-Enrolment

The expansion of Auto-Enrolment has already been put into place. These changes include lowering the starting age from 22 to 18 and having pension contributions begin from the first penny earned, rather than the current starting point of _lower_earnings. This should give young savers a boost in the long term.

4. Help savers understand retirement income options

Under the 2015 ‘pension freedoms’ savers can choose how they withdraw from their pension. But with life spans growing longer, it’s more important than ever for pension savings to support individuals throughout their whole retirement. One idea is requiring pension schemes to clearly outline withdrawal options.

5. Improve self-employed pension saving

Currently just 16% of self-employed workers pay into a pension, causing millions to retire without adequate savings. This has the potential to put additional pressure on the future State Pension, so the government may need to consider how they could expand Auto-Enrolment to engage more self-employed workers.

6. Pot for life reforms

The idea of ‘pot for life‘ is to provide workers with more control over their retirement savings. Traditionally, when someone changes jobs, their new employer selects a new pension scheme for them. Over time, this leads to multiple pension pots scattered across various providers.

It’s already technically possible to ask an employer to pay into a personal pension of your choice, rather than to use the Auto-Enrolment provider offered by them. But, employees rarely ask their employers to do this - and few employers agree. So far, the new government has made no commitment on pot for life.

7. Reallocate funds into the UK economy

The previous government announced plans to stimulate economic growth by encouraging investment in UK companies from UK pension funds. Labour has signalled they support this reform. However, of all the pension recommendations, this policy has been met with a high level of criticism.

8. Reviewing the minimum pension age

Currently the earliest you can access your private or workplace pensions is from age 55 (rising to 57 in 2028); while you’re currently eligible for the State Pension from age _state_pension_age (rising to _pension_age_from_2028 by 2028). One proposed change is reviewing the minimum pension age, potentially improving retirement fund sustainability. It’s worth noting that such policy moves are often unpopular with the general public.

9. Unveil the long-awaited pensions dashboard

Back in 2002, the Secretary of State for Work and Pensions suggested a web-based retirement planning tool. Fast forward over two decades and this still hasn’t been implemented. The pensions dashboard would allow savers to view their combined pensions information online, helping to reconnect lost pension pots and better plan for retirement.

PensionBee’s VP Public Affairs, Becky O’Connor, commented: “We’re pleased to welcome the new Pensions Minister. This will be a crucial appointment, given Labour’s manifesto commitment to a comprehensive review of the pensions and retirement savings system, a measure that could potentially benefit millions of savers.”

Summary

With the appointment of Emma Reynolds as the Pensions Minister in the new government, there’s a renewed sense of hope for positive changes in the way pensions are managed.

This is part of our monthly pension update series. Check out the next month’s summary here: What happened to pensions in August 2024?

Have a question? Get in touch!

Do you want to know more about your pension plan with PensionBee? You can check out our Plans page to learn how your money is invested in different assets and locations, or log in to your BeeHive to see your specific plan. You can always send comments and questions to our team via [email protected].

Risk warning

As always with investments, your capital is at risk. The value of your investment can go down as well as up, and you may get back less than you invest. This information should not be regarded as financial advice.

Period | Market Event | FTSE World TR GBP (%) | 4Plus Plan (%) |

|---|---|---|---|

4Plus Plan’s inception – 6 Sept 2013 | QE Tapering, China Interbank Crisis and its aftermath | -5.44 | -2.41 |

3 Oct 2014 – 15 May 2015 | Oil price drop, Eurozone deflation fears & Greek election outcome | -5.87 | -1.77 |

7 Jan 2016 – 14 Mar 2016 | China’s currency policy turmoil, collapse in oil prices and weak US activity | -7.26 | -1.54 |

15 June 2016 – 30 June 2016 | BREXIT referendum | -2.05 | -1.07 |