The Next Generation of Retirees Report

2020 was one of the most challenging years in recent times, but little is known about the long-term impacts on people's financial goals. Our latest research shows millions of people across the UK are reassessing crucial aspects of their lives, including their retirement. From record numbers of unemployment, to furlough resulting in millions taking home 80% of their regular income, many have been forced to consider what implications this may have on their future.

PensionBee's recent survey reveals how each of the current working generations have been affected by the COVID-19 pandemic, including Generation Z (18-23 years old), Millennials (24-40 years old), and Generation X (41-54 years old). We surveyed 2,000 people from across the UK to find out how attitudes towards saving for retirement might have changed since March 2020. We've shown results by generation and region to gain a better understanding of how people may be impacted differently.

How has COVID-19 impacted retirement

plans and pension savings?

Out of those surveyed, 43% said they’d be forced to delay their retirement due to the pandemic. This means as many as 13.5 million Brits will be forced to work longer than they’d planned, to make up for the impact COVID-19 has had on their finances.

What percentage of each generation plan to delay their retirement?

How long does each generation plan to delay retirement for?

The generation closest to retirement, Generation X, were the least likely to delay, with only 1 in 3 (35%) stating their plans had to be pushed back. In contrast, over half (52%) of Millennials said the pandemic would impact their retirement, and despite being early in their careers, two thirds (67%) of those from Generation Z agreed.

The average length of the expected delay is 18 months, however this does vary amongst each generation. Generation X expects a delay of 17 months, compared to 20 months for Millennials, and 24 months for Generation Z.

Overall, more than 1 in 10 (13%) respondents said they’ve been financially impacted by the pandemic. But despite these difficulties, they’d found opportunities to save in the last twelve months.

This was most relevant for Millennials who managed to save the most each month, averaging £336. Generation Z saved slightly less, averaging £316. On the other hand, Generation X saved far less, averaging just £218. This could perhaps be explained by Generation Z, and potentially some Millennials¹, being far more likely to be living at home with less financial commitments, such as rent, a mortgage, or car repayments.

Per month, how much has each generation been able to save?

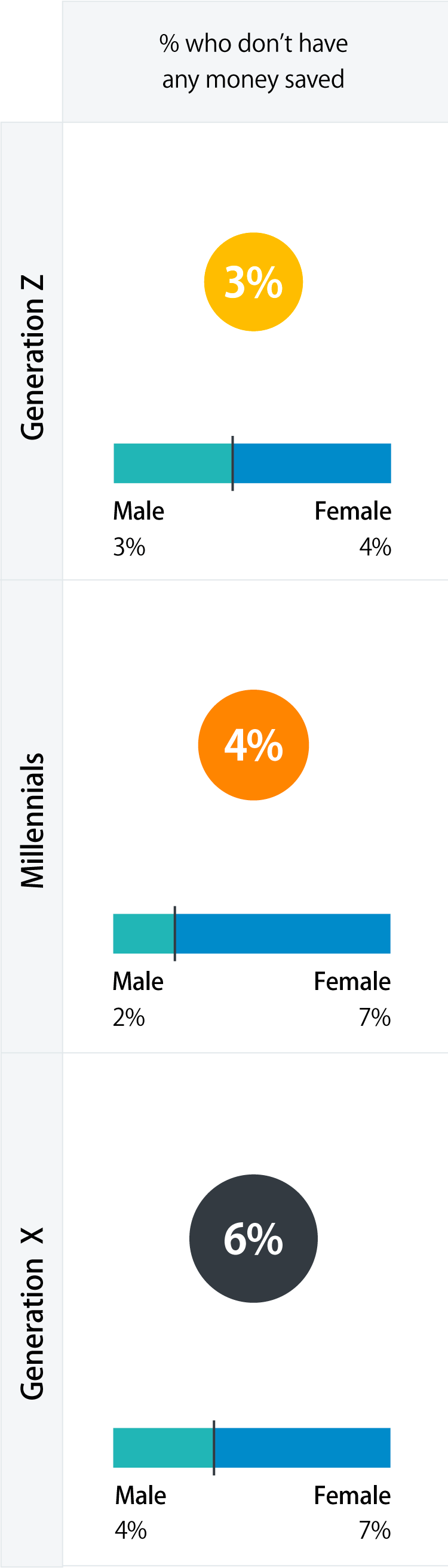

What percentage of each generation hasn’t been able to save anything during

the

pandemic?

Which industries are facing the longest retirement delays due to Covid-19

In addition to intergenerational differences, disparities in retirement timelines can be seen across various industries. Those working in Sales, Media and Marketing fear they will have to work an extra 30 months compared to their counterparts — higher than any other industry. With most jobs in this industry being classed as ‘non-essential’, many office workers spent the first lockdown on furlough, or taking a pay cut in an attempt to keep businesses afloat.

The second hardest hit industry was Art and Culture, one of the industries most discussed in the media due to limited help offered by the government. Those who work in theatres, museums, cinemas and galleries—along with tens of thousands of entertainers—fear they will have to delay their retirement by 29 months.

The third longest delay was for those who work in IT and Telecommunications at 28 months, followed by the Legal profession at 25 months, and Architecture, Engineering and Building at 24 months. Each of these industries were affected by the first lockdown, but have since been able to operate as usual, with the legal profession in particular, facing significant backlogs in cases.

For those who work in healthcare, there was no other choice than to keep operating at such a crucial time. This industry expects the shortest retirement delays, but it is still forecasting an additional 12 months of work.

Industries that will be delaying their retirement by the most years*

How much does each generation have in

their savings pot for retirement?

Generation X have the largest average pension pots, at £33,547. Millennials follow with an average of £22,049. Generation Z follow closely with an average of £21,765, perhaps explained by the introduction of Auto-Enrolment, resulting in this age bracket being part of their workplace pension for a longer period than their counterparts. Generation Z appear on track to retire with larger pension pots than both Millennials and Generation X. However, Generation Z may not have the same disposable income as other generations as salary growth continues to lag behind house prices, new cars and other major purchases.

Younger generations may also focus their efforts on saving for other large expenses, such as weddings, deposits for a home, or raising children. Whereas those from Generation X are more likely to already be married or in a civil partnership, own their home, and have older children that have flown the nest.

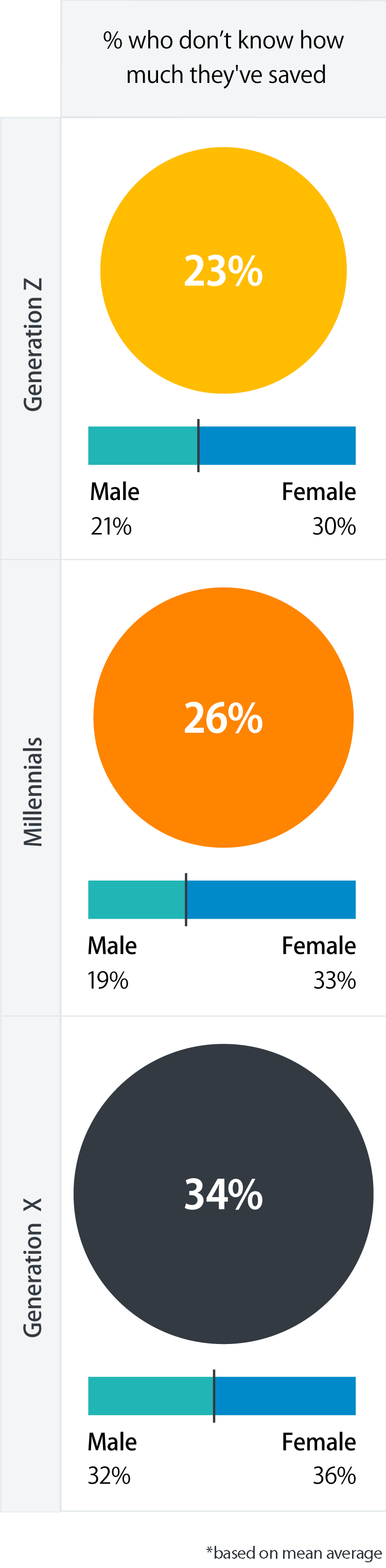

Despite having the largest average pension pots and being closest to retirement, more than 1 in 3 (34%) from Generation X are unsure about much they’ve saved towards retirement. In comparison, just over a quarter of Millennials (26%) claimed this. Generation Z appears the most clued up when it comes to the size of their retirement pot, with just 23% of respondents not knowing how much they’ve saved.

Only a small proportion of Generation Z (3%) and Millennials (4%) admitted that they don’t have any money saved towards retirement. However, this is smaller than the number of Generation X (6%) respondents who said the same.

How much does each generation have in their pension pots?

Average pension pot sizes across the UK

After considering both intergenerational and industry differences, location can play an important factor in an individual’s retirement pot due to large wealth disparities within the UK.

Our research found the highest average pension saving is in Edinburgh, at £82,000. Meanwhile, just 45 miles away, Glaswegians have the smallest pension savings at £22,900. Notably, the average salary in Edinburgh is £31,0002, just £2,0003 more than Glasgow.

On further evaluation of English cities, the largest average pension savings were found in Southampton at £58,900. The city with the smallest average saving was Norwich at £30,300. Despite London having the highest average salary in the UK (£38,000), Londoners only have the eighth highest average pension pots at £42,299. This is possibly explained by the high cost of living within the capital.

What are the average pension savings pot sizes across the UK?

Lifestyle decisions and retirement planning

The financial repercussions of the pandemic and the heightened anxiety around what this will mean for the future have left some questioning whether they’ll be able to retire at all.

What percentage of each generation feel they won't be able to live comfortably in retirement?

Younger generations will have to work longer than any other age group in history due to the ongoing rise in state retirement age. But despite this, 12% of Millennials feel they won’t be able to live comfortably in retirement, with 5% of those in Generation Z agreeing.

These concerns extend to the older generation, with 16% of Generation X’s admitting they won’t be able to fund their preferred lifestyle. This is assumed to include large expenses such as monthly car payments and annual holidays abroad, but could also cover smaller expenses such as day trips, meals at restaurants and television subscription services.

For those on the cusp of retirement, reservations are understandable. The State Pension currently pays £179.60 per week. For many, this may not be enough to cover expenses. In some cases, individuals may still be tied down to the latter end of a mortgage, or lack clarity on the size of their savings, causing concern about how they’re going to fulfil their financial commitments. This may leave some individuals feeling like they have no other option than to delay their retirement.

With personal pensions only accessible at 55 (rising to 57 in 2028) and the State Pension receivable on your 65th birthday, each generation was also asked what they think is the ideal age for retirement.

What’s the perfect age to retire?

Overall, the three generations widely agree on a retirement age of late 50s to early 60s. Generation Z think we should be hanging up our working boots at 57, whilst Millennials would prefer to hang theirs at 58. Generation X, however, prefers the idea of working a little longer, saying the ideal age to retire is 61 - which, for some of that generation, is as little as seven years away.

It’s also possible that as Generation X approaches retirement age, they may not be in a position where they can financially support themselves. Or, quite simply, they don’t feel old enough.

The thought of working so late in life is clearly far more unappealing to the youngest generations. 10% of Generation Z said they’re considering not having children so they can afford to retire early, compared to just 4% of Millennials.

Are younger generations making big lifestyle decisions now when planning for retirement?

The idea of not having children to bring forward retirement is most popular with London residents, where 5% of respondents across all generations stated this. In comparison, there wasn’t a single respondent in the North East who cited not having children as a way to bring forward their retirement.

For those earning between £25,001 and £55,000, not having children was something they’d be more likely to consider than their lower-earning counterparts.

Based on these responses alone, it appears you’re more likely to consider not having children for financial benefit if you’re living in London with an average to higher paid job. Factors such as the cost of childcare, reliance on public transport, and small, expensive properties within London may contribute towards this decision.

It’s never too soon - or too late - to start preparing for your retirement

For many of us, the State Pension won’t be enough to continue living to the same standard we might have become accustomed to during our working lives. So now is the time to think about saving for our future.

Consider these tips when thinking about your pension and what it means for you:

- Calculate how much you have and how much you need - It’s estimated most people will need about 70% of their salary to live comfortably in retirement, but the amount you’ll require largely depends on your circumstances and lifestyle. It’s important to think about how much you can afford to save, how long you’ve got until you retire and your desired retirement income.

- Start saving sooner rather than later - The earlier you start saving into a pension, the more time it will have to grow. If you leave your pension untouched for several decades, a small savings pot is likely to turn into a much bigger pot by the time you retire, thanks to compound interest.

- Check your State Pension entitlement - Currently, all workers need to have paid National Insurance Contributions for at least 10 years to qualify for the State Pension. To receive the full amount of £179.60 per week (2021/2022) you’ll need to have paid for at least 35 years.

- Find your old pensions - If you’ve had multiple jobs in your career, you may have been enrolled in various workplace pension schemes. If you’re unsure, try the government’s Pension Tracing Service. Alternatively you can contact your old employers for help or ask your new pension provider for assistance.

- Consolidate your pensions into one plan - This will make your savings easier to manage and help prevent you from losing track of your hard-earned money from previous jobs. In addition, you’ll only pay fees on one larger pension pot, rather than paying multiple fees on a range of smaller pots.

- Make sustainable withdrawals - It may be beneficial to think about any future withdrawals in percentage terms, rather than pounds and pence. If you set a percentage figure for your withdrawals, these automatically reduce in size when markets are lower. This adjustment in thinking should help you to avoid cashing in too much of your pension too soon.

Methodology

PensionBee surveyed 2000 UK citizens in March 2021 about their pension pot savings, their retirement plans and the financial impact of COVID-19 on their retirement savings. The data was then segmented via three generations - Generation Z (18 - 23 years old), Millennials (24 - 40 years old) and Generation X (41 - 54 years old) - to understand each generation's financial and lifestyle plans for retirement.

Survey data is available upon request. Page last updated: March 2021.

Footnotes

- The Guardian: https://www.theguardian.com/society/2020/oct/18/boomerang-trend-of-young-adults-living-with-parents-is-rising-study#:~:text=Around%203.5%20million%20single%20young,of%20the%20coronavirus%20pandemic%20deepens.

- PayScale.com: https://www.payscale.com/research/UK/Location=Edinburgh-Scotland%3A-Edinburgh/Salary

- PayScale.com: https://www.payscale.com/research/UK/Location=Glasgow-Scotland%3A-Glasgow/Salary